How to Get a Mortgage: Step-by-Step Guide for First-Time Home Buyers

Last updated on June 3, 2026

Learn how to get a mortgage for first-time home buyers.

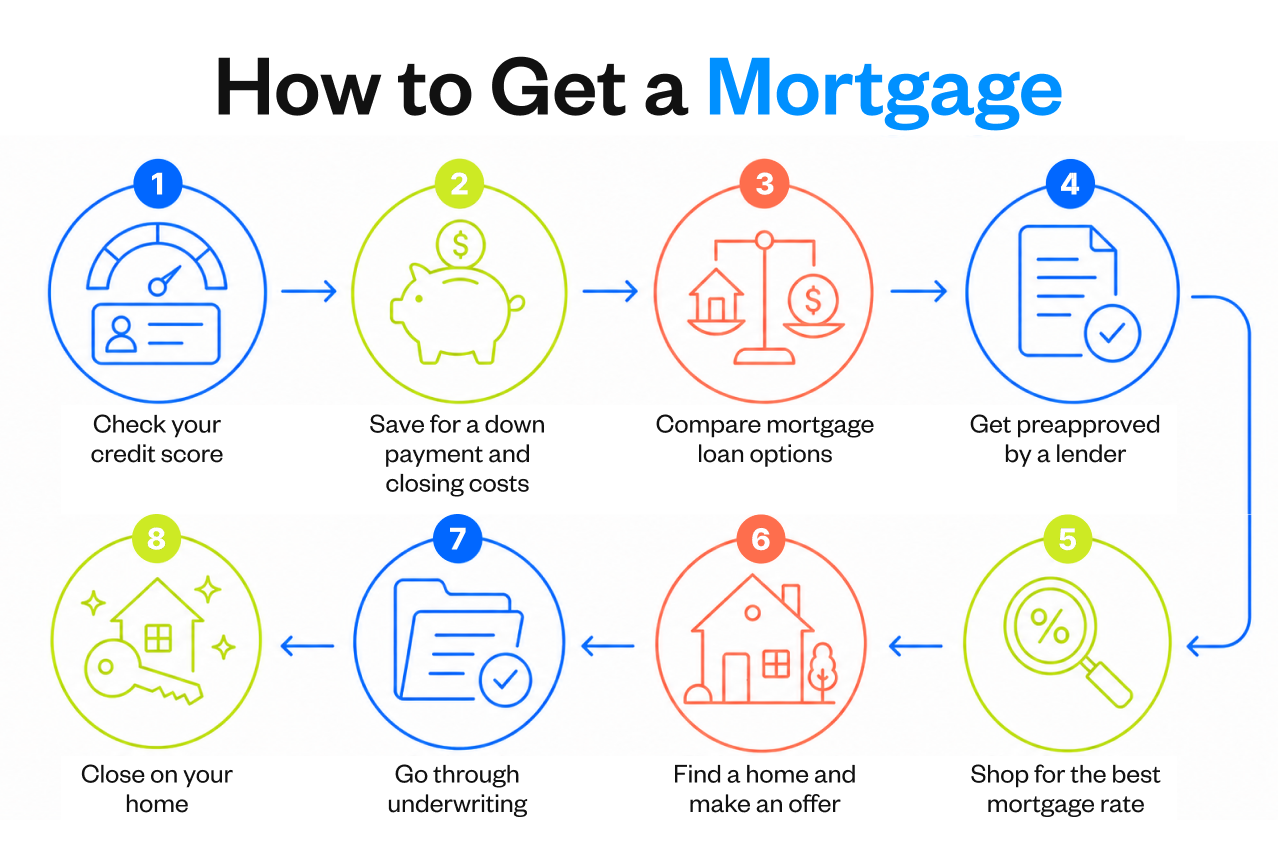

To get a mortgage, you will need to assess your credit score, save for a down payment and closing costs, compare mortgage types, get pre-approved by a lender, shop for a mortgage, find a home, go through underwriting and close on your home.

Whether you’re buying your first home or starting to explore your options, this guide walks you through qualifying requirements, loan types and every step from pre-approval to closing day. By the end, you’ll have a clear roadmap for securing a mortgage loan that fits your financial situation.

Key Takeaways

- Most mortgage lenders require a minimum credit score of 580-640 to qualify for a mortgage, though a higher score can help you get a better interest rate. California Credit Union generally has a minimum score of 640

- Down payments range from 3% to 20% of the price of the home for most mortgage types

- Getting pre-approval before house hunting gives you a clear budget and shows sellers you’re a serious buyer

- Comparing rates from multiple lenders can save you thousands over the life of your loan

- First-time home buyers may qualify for assistance programs that reduce upfront costs

What Is a Mortgage?

A mortgage is a loan you take out to buy a home. You borrow money from a lender, and the home itself serves as collateral, meaning the lender can take the property if you stop making payments.

Your monthly payment is made up of four components, often called PITI:

- Principal: The amount going toward your loan balance

- Interest: What the lender charges for borrowing money to purchase your home

- Taxes: Property taxes, which are usually held in escrow

- Insurance: Homeowners insurance and, in some cases, private mortgage insurance (PMI)

One of the first decisions you’ll need to make is choosing a fixed-rate or an adjustable-rate mortgage (ARM). A fixed-rate mortgage locks in the interest rate for the entire loan, keeping your payment predictable. An ARM starts with a lower rate for a set period — often five or seven years — then adjusts based on market conditions.

You’ll also decide on a loan term. A 30-year mortgage means lower monthly payments, while a 15-year mortgage comes with higher payments but less interest paid overall. Use our 15 vs. 30-year mortgage calculator to compare your options.

What Do You Need to Qualify for a Mortgage?

Before you apply, it helps to know what lenders evaluate. Here are the main areas they look at:

Credit score requirements

Most conventional mortgage loans require minimum credit scores of 620-640. At California Credit Union, we generally have a minimum FICO of 640. A higher FICO score typically gets you better rates, which means saving more over the entire life of your loan.

Income and employment history

Lenders want to see steady income to trust that you can make your monthly mortgage payments on time. They typically look for at least two years of consistent employment, verified through pay stubs, W-2s and tax returns.

Debt-to-income (DTI) ratio

This percentage compares your total monthly debt payments to your gross income. Most lenders prefer between 36% and 43% or lower.

Savings requirements

Beyond down payment and closing costs, lenders like to see at least a few months’ worth of mortgage payments in cash reserves.

How to Get a Mortgage: Step-by-Step

The mortgage process involves several stages, each building on the last. Here’s what to expect from start to finish:

1. Check your credit score

Your credit score plays a direct role in whether you get approved and what rate you’re offered. Pull your credit report and review it for errors like incorrect balances or unfamiliar accounts, both of which can lower your score.

If your score is low, focus on paying down credit card balances, making all payments on time and avoiding new credit applications. Learn more about what qualifies as a good credit score.

2. Save for a down payment and closing costs

How much you need for a down payment depends on the loan type. The most common type, conventional loans, require 3% to 20% down. If you put down less than 20% on a conventional loan, you’ll pay PMI, which is an added monthly cost to keep in mind.

Closing costs typically range between 2% and 5% of the purchase price and cover origination charges. Use our closing cost calculator to estimate what you’ll owe.

First-time home buyers can also qualify for down payment assistance through grants, forgivable loans or matched savings programs. Check with your state housing authority or lender for available options.

3. Compare mortgage loan options

Not all mortgages work the same way. Here are the most common types:

- Conventional loans: Not backed by a government agency, these generally require a credit score of 620-640 and at least 3% down

- VA loans: Available to eligible veterans, active-duty service members and surviving spouses with zero down payment and no PMI

4. Get pre-approved by a lender

A pre-approval letter tells you how much a lender will potentially let you borrow based on a review of your finances. You’ll need recent pay stubs, W-2s or 1099s from the past two years, tax returns, bank statements and a valid ID. The lender will also run a hard credit inquiry.

Getting approved before you tour homes gives you a realistic price range and makes your offer stronger in a competitive market. At California Credit Union, we also offer the option complete your application 100% digitally.

5. Shop for the best mortgage rate

Even a small difference in interest rates adds up to thousands of dollars over the life of the home loan, so get quotes from at least three to four lenders.

Compare the annual percentage rate (APR) when looking at offers, not just the interest rate. The APR factors in fees and gives a more accurate picture of total borrowing cost. A mortgage payment calculator can show how different rates affect your monthly payment.

Credit unions offer the most competitive mortgage rates and lower fees, so it’s worth comparing a bank vs. credit union mortgage loan.

6. Find a home and make an offer

A real estate agent can give you better access to listings, market insights and negotiation support. Your offer will typically include contingencies, which are conditions that must be met for the sale to go through, such as a home inspection, appraisal and financing contingency.

Use an income required for a mortgage calculator and home affordability calculator to confirm the purchase fits your budget before making an offer.

7. Go through underwriting

After your offer is accepted, your lender’s underwriting team verifies your income, assets, credit and the property’s value through an appraisal. This stage can take a few weeks.

8. Close on your home

Closing day is when everything becomes official. You’ll sign the mortgage note, deed of trust and other documents then pay your closing costs and remaining down payment.

Before signing, review the Closing Disclosure form carefully. This document outlines your final loan terms, monthly payment and all fees. Once everything is signed and funded, you’ll get the keys to your new home!

Common Mortgage Mistakes for First-Time Home Buyers

Even well-prepared buyers can make simple mistakes during the mortgage process. Here are the most common mistakes to watch for:

- Not getting pre-approved early: Waiting to get pre-approved can slow everything down once you find a home you want

- Overextending budget: Qualifying for a certain amount doesn’t mean you should borrow that much. Factor in maintenance, utilities and other costs beyond your mortgage payment

- Ignoring total loan cost: A low monthly payment can be misleading if the term is longer or the rate is higher. Look at what you’ll pay over the full life of the loan

- Opening new credit during the process: New debt during underwriting can change your DTI ratio and jeopardize your approval, such as opening a new credit card or getting an auto loan

- Skipping rate comparisons: Accepting the first rate you’re offered can cost you thousands over time. Compare lenders to ensure you get the best rates and terms

Wrapping Up: How to Get a Mortgage

Figuring out how to get a mortgage doesn’t have to be stressful. With a solid credit score, savings in place and a clear understanding of your loan options, you can move through the process with confidence.

California Credit Union offers home loan products for first-time and experienced buyers alike. From competitive rates to personalized guidance from local lending experts, we're here to support you at every step of the homebuying journey.

Federally Insured by NCUA. Equal Housing Opportunity. NMLS #401403

All loans are subject to approval, including credit approval and membership eligibility. Rates, terms and conditions are subject to change and available at ccu.com.