What Do You Need to Open a Bank Account? A Complete Guide

Last updated on March 16, 2026

Discover What You Need to Open a Bank Account

To open a bank account, you will need a government-issued photo ID, such as a driver’s license, proof of residency, such as utility bills and your Social Security number. Additionally, you will need to meet certain eligibility requirements set by the bank or credit union, such as age requirements, residency or citizenship status and initial deposit requirements.

Opening a bank account is one of the most important steps toward building a solid financial foundation, whether you’re managing day-to-day expenses, setting money aside, or learning how to save money for a specific goal. This guide walks you through everything you need, from the right account type to the documents you’ll need on day one.

Key Takeaways

- Opening a bank account requires a government-issued photo ID, proof of where you live and your Social Security number.

- Most financial institutions require applicants to be at least 18 to open an account independently, though teens can often open accounts with a parent or guardian.

- The documents required to open a new bank account vary slightly by account type, but the core requirements are standard across most institutions.

- Non-residents can often open a U.S. bank account, though it typically requires extra documentation like a passport, visa, and ITIN (Individual Taxpayer Identification Number).

- Most banks and credit unions now let you open an account entirely online, often with your account active within one to two business days.

Types of Bank Accounts You Can Open

Before gathering your paperwork, it helps to know which type of account you’re opening. Not sure which fits your situation? Understanding the difference between a checking vs. savings account is a good place to start. Each type of bank account serves a different purpose and shapes how you’ll use and access your money.

Checking Account

A checking account is built for everyday spending, including bills, purchases and day-to-day cash flow. Most come with a debit card and online banking access.

Savings Account

A savings account is where you place money you don’t plan to spend right away. These accounts may earn interest over time, especially once compound interest starts working in your favor.

Money market Account

A money market account combines features of checking and savings, often offering higher interest rates along with limited check-writing privileges.

Student, teen, and joint Accounts

These accounts are designed for younger holders or people opening an account alongside someone else. They often come with lower minimums and parental oversight options.

Business Accounts

A business account keeps personal and business finances separate. Requirements tend to be more involved, typically including business registration documents and an EIN (Employee Identification Number).

Common Eligibility Requirements to Open a Bank Account

Whether you’re opening your first bank account or learning how to switch banks and start fresh somewhere new, the eligibility requirements are largely the same. Here’s what to expect before you apply:

- Minimum age requirements: Most financial institutions require applicants to be at least 18 to open an account independently. Minors can often open accounts with a parent or guardian, which is a common path for anyone opening their first bank account

- Residency or citizenship status: Many credit unions and banks require a U.S. address, though non-residents may still qualify with additional documentation

- Ability to provide identifying information: You’ll need to verify your identity with an accepted form of ID. This is a federal requirement, not just a bank policy

- Credit history considerations: Most checking and savings accounts don’t require a credit check, but your credit union or bank may review your ChexSystems report, which tracks past banking activity

- Opening deposit requirements: Some accounts require a minimum deposit, while others have no minimum at all

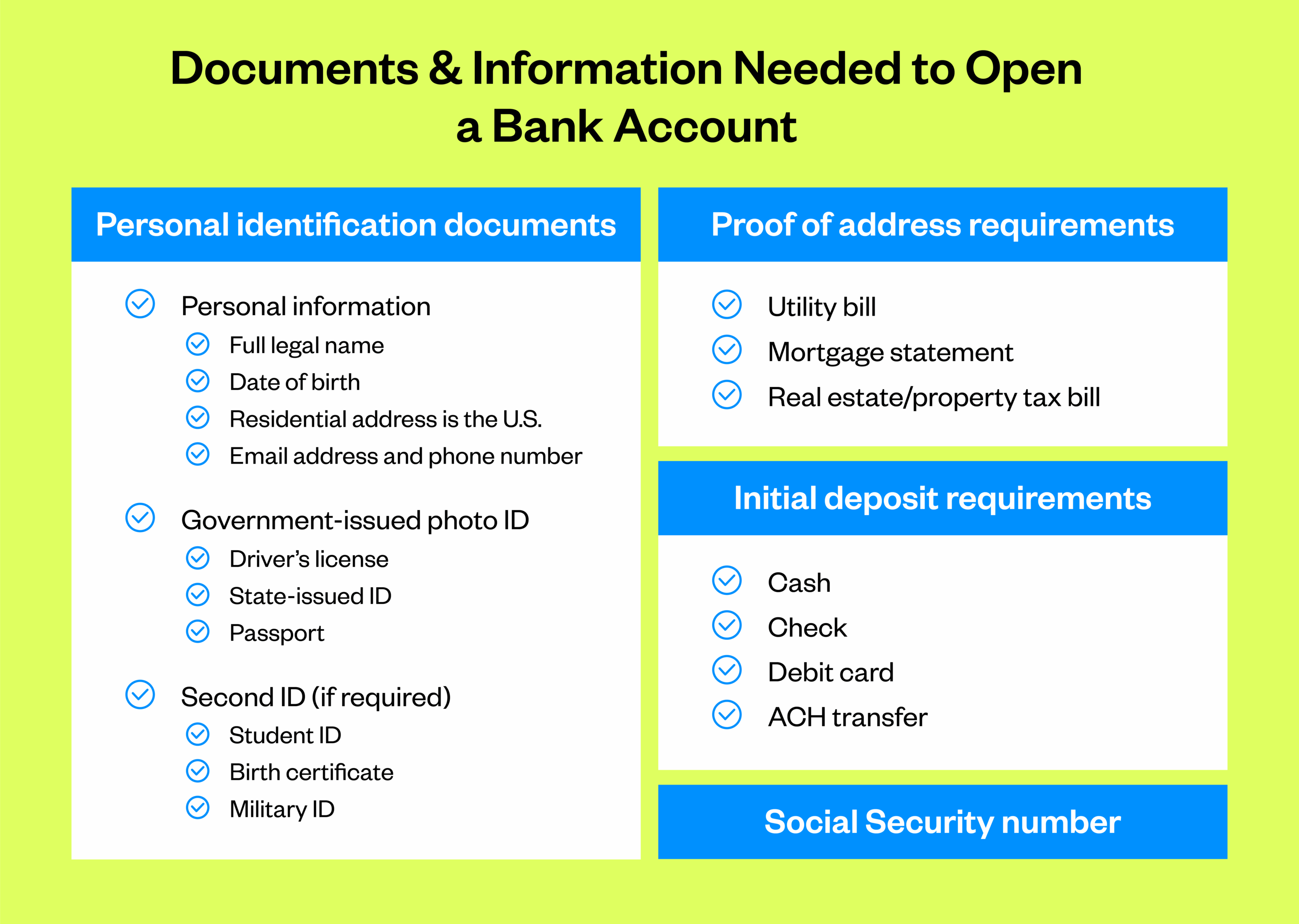

Documents Needed to Open a Bank Account

Knowing the documents required to open a new bank account before you show up saves you from making two trips. Most banks and credit unions ask for the same core items.

Personal identification documents

You’ll need at least one government-issued photo ID. Some institutions may request a second form as well. Here are the most widely accepted options:

Government-issued photo ID: Driver's license, state-issued ID or Passport

Second ID (if required): Student ID, Birth certificate or Military ID

Proof of address requirements

Banks need to confirm where you live. The documents typically accepted include a utility bill, mortgage statement or real estate/property tax bill.

If you don’t have bills in your name, which is common for students or those living with family, some institutions will accept a parent or guardian’s proof of address alongside documentation that connects you to that address. If you’re renting, a signed letter from your landlord may also be accepted. Policies vary, so call ahead to confirm what your institution requires.

Social Security number

Banks are required by federal law to collect your Social Security number (SSN) when you open an account. This is because the USA PATRIOT Act requires all banks and credit unions to verify the identity of anyone opening an account as a safeguard against fraud, money laundering, and terrorism financing.

If you don’t have an SSN, some banks will accept an Individual Taxpayer Identification Number (ITIN). The IRS issues ITINs for individuals who aren’t eligible for an SSN, and they serve the same tax reporting function. Confirm whether your institution accepts ITINs before your visit.

Initial deposit requirements

Funding your account is usually the final step. Many accounts have no minimum deposit, while others may ask for anywhere from $25 to $100. At California Credit Union, some accounts can be opened with as little as $0.01. The most common ways to fund an account include cash, check, debit card or ACH transfer.

Wrapping Up: Gathering Documentation to Open a Bank Account

Knowing what you need to open a bank account before you apply makes the process faster and less stressful. For most people, that means a government-issued photo ID, proof of address, a Social Security number and an initial deposit.

At California Credit Union, we make it straightforward to get started. Whether you’re opening a checking account for daily spending or a savings account to work toward your goals, discover the benefits of banking with a member-owned institution.