Roth IRA vs. Traditional IRA: Which Retirement Account Is Right for You?

Last updated on March 10, 2026

Retirement planning can be complicated, especially when you’re trying to figure out which savings vehicle works best for your situation. Two of the most popular options are the Roth IRA and traditional IRA, and while they share some similarities, the difference between them can significantly impact your financial future.

Understanding how each account works will help you make an informed decision about where to put your retirement savings. Just as learning how to save money in your everyday life builds good financial habits, choosing the right retirement account sets you up for long-term success.

Key Takeaways

- Traditional IRAs may allow you to take a tax deduction now, while Roth IRAs provide tax-free income in retirement. With Roth IRAs you never pay taxes on the earnings. This may be a significant tax savings if you start contributing at a young age and continue contributing until you retire

- Your tax bracket now and in the future plays a major role in choosing between a Roth and traditional IRA. If you anticipate that you will be subject to a higher tax rate in the future, this tends to favor a Roth IRA. On the other hand, if you expect to be in a lower tax bracket, a Traditional IRA may be the right choice

- These retirement account types have the same contribution limits for 2026 - $7,500

- Contributing to a Roth IRA has income restrictions, but contributing to a Traditional IRA is available to anyone with earned income. Traditional IRAs no income limits to contribute but you may not qualify for a tax deduction if you or your spouse participate in an employer-sponsored retirement plan and your income is above a specified threshold

- If eligible, you can have both types of retirement accounts, but your total contributions across all IRAs cannot exceed the annual limit set by the IRS

- With traditional IRAs, you must take minimum distributions when you turn 73 based on the balance of your Traditional IRA (contributions + earnings). These minimum distributions will be added as income when you file your tax return. Roth IRAs do not have this requirement

What Is an IRA?

An individual retirement account (IRA) is a savings account that’s tax-advantaged and helps you build wealth for retirement. Unlike employer-sponsored plans like a 401(k) or 403 (b) that depend on your workplace offering them, individual retirement accounts are available to anyone with earned income. You open an IRA on your own through a financial institution, giving you more control over your investment choices.

IRAs encourage long-term savings by offering tax benefits you won’t find in regular investment accounts. Whether you choose a Roth or traditional IRA, your investment can grow through compound interest. This growth potential can add up substantially over decades of saving.

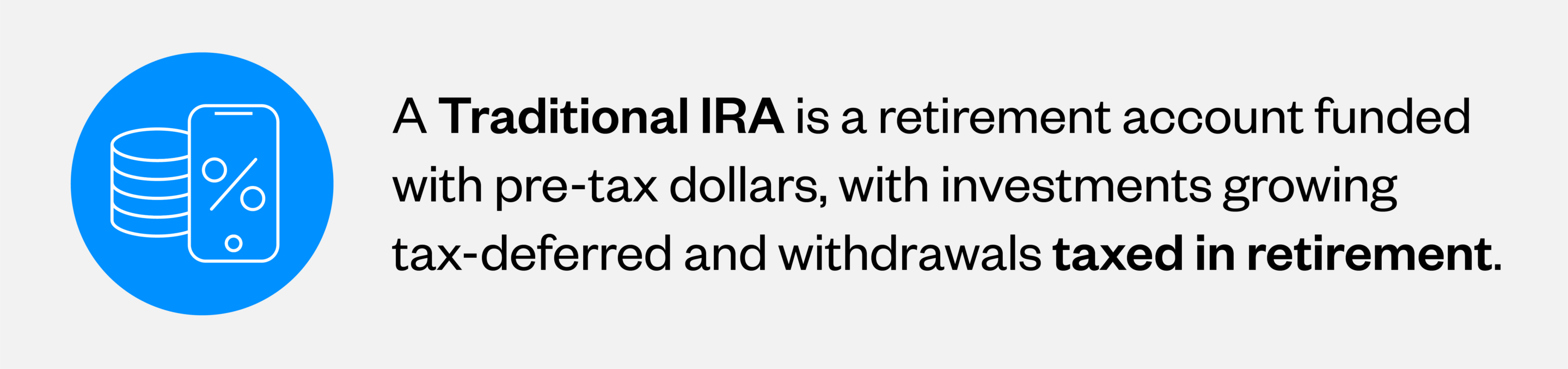

What Is a Traditional IRA?

A traditional IRA lets you contribute money to your retirement account on a pre-tax basis, meaning you may get to deduct what you contribute from your taxable income. For example, if you earn $70,000 and contribute $5,000 to a traditional IRA, you might only pay taxes on $65,000 of income that year.

Your money grows tax-deferred, which means you won’t owe taxes on investment gains, dividends or interest until you take the money out of the account in retirement. This pre-tax structure differs from investing with after-tax dollars in a regular brokerage account. When you eventually take distributions from a traditional IRA in retirement, those withdrawals get taxed as ordinary income.

Tax benefits of a Traditional IRA

The main reason people choose traditional IRAs is the potential for an immediate tax deduction. If you’re eligible to deduct your contributions, you can lower your taxable income today, which might drop you into a lower tax bracket or increase your refund. These upfront tax savings can be valuable if you’re in your peak earning years and facing higher tax rates now than what you expect to pay in retirement.

The traditional IRA deductibility rules and income limits determine whether you can claim this deduction. Additionally, the ability to deduct contributions depends on whether you or your spouse participates in a retirement plan at work.

Traditional IRA deduction limits

If neither you nor your spouse has access to a retirement plan at work, you can deduct your full traditional IRA contribution regardless of your income. However, if you or your spouse are covered by a workplace plan, the deductibility of your contributions starts to phase out at certain income levels.

It’s important to understand the difference between contributing and deducting. You can put money in a traditional IRA regardless of how much you earn, but you might not be able to deduct those contributions if your income is too high and you have workplace retirement plan coverage.

Traditional IRA contribution limits

The IRA contribution limits change each year based on inflation adjustments. Here’s what you can contribute:

For the 2026 tax year:[2]

- Standard contribution limit: $7,500

- Catch-up contribution (age 50+): Additional $1,100

- Total limit for those 50+: $8,600

Keep in mind that these limits apply to all your IRA contributions across all traditional and Roth accounts combined.

Traditional IRA withdrawal rules

When you start taking money out of your traditional IRA in retirement, those distributions are taxed as regular income. Once you reach age 73, you’re required to take minimum distributions (RMDs) each year, whether you need the money or not. The IRS calculates these RMDs based on your account balance and life expectancy.

Pro tip: Use our retirement savings calculator to determine how long your savings will last based on your withdrawal strategy.

If you withdraw money from your account before age 59½, you’ll likely face a 10% early withdrawal fee in addition to regular income taxes. That said, there are exceptions for certain situations like first-time home purchases, qualified education expenses or disability. The early withdrawal penalties for a traditional IRA can be costly, so it’s generally best to leave the money untouched until retirement.

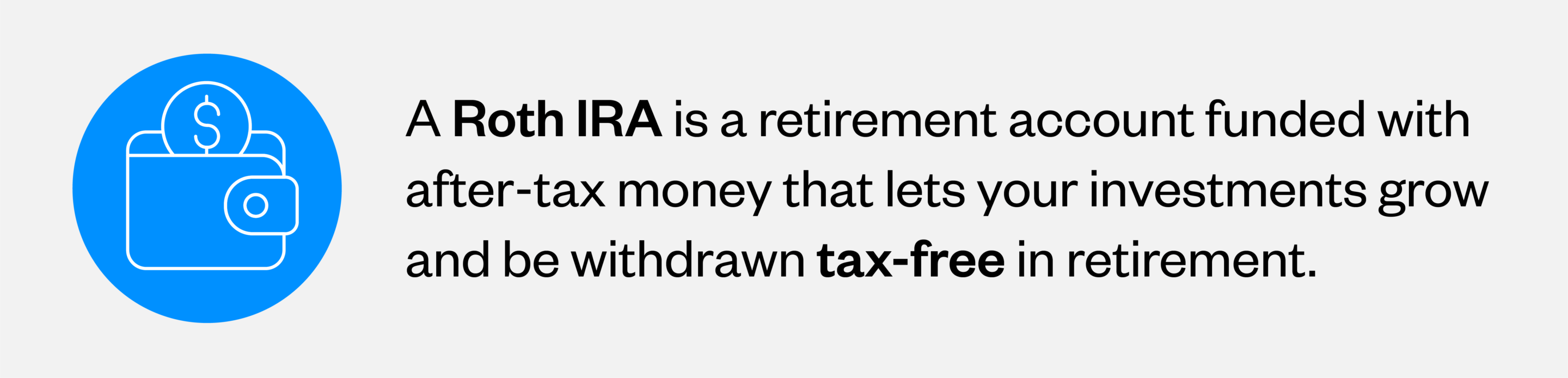

What Is a Roth IRA?

With a Roth IRA, you contribute money that’s already been taxed, so you don’t get an upfront tax deduction. However, that means that your investments grow tax-free, and you can withdraw both contributions and earnings tax-free in retirement once you’re 59 ½ and have held the account for at least five years.

Since you’ve already paid taxes on the money going in, the IRS won’t tax you again when you take it out. This after-tax contribution structure means you’re essentially locking in your current tax rate rather than gambling on what rates might be when you retire.

Tax benefits of a Roth IRA

The major advantage of a Roth IRA is tax-free income in retirement. When you’re 70 or 80 years old, for example, and need to cover living expenses, being able to withdraw money without owing the IRS anything can provide tremendous financial flexibility. This benefit is especially helpful if tax rates increase in the future, since you’ve already locked in today’s lower rates. It also helps if your other retirement income sources put you in a higher tax bracket because Roth withdrawals don’t count as taxable income and won’t push your tax burden even higher.

Roth IRA income limits

Unlike traditional IRAs, eligibility for Roth IRAs based on income can prevent higher earners from contributing directly. For 2026, contribution limits start to phase out at $153,000 for single filers and $242,000 for married couples filing jointly. Once your income exceeds $168,000 (single) or $252,000 (married filing jointly), you can’t contribute to a Roth IRA at all.

High earners who want the benefits of a Roth IRA can use what’s called a backdoor Roth IRA strategy. This involves first contributing to a traditional IRA (which has no income limits) and then later converting it to a Roth IRA. It’s worth discussing this approach with a tax professional first, as the conversion can have tax implications.

Roth IRA contribution limits

The contribution limits for Roth IRAs match those for traditional IRAs and often change annually. Here’s what you can contribute:

For the 2026 tax year:[2]

- Standard contribution limit: $7,500

- Catch-up contribution (age 50+): Additional $1,100

- Total limit for those 50+: $8,600

Remember, these limits apply across all your IRA accounts combined. If you contribute $4,000 to a Roth IRA in 2026, you can only put $3,500 into a traditional IRA that same year.

Roth IRA withdrawal rules

If you’ve had your Roth IRA for at least five years and you’re over 59½, you can withdraw everything tax-free and penalty-free.

Before retirement, Roth IRAs offer more flexibility than traditional IRAs when it comes to accessing your money. You can withdraw your contributions (the original money you deposited) anytime without taxes or penalties because you already paid taxes on that money. However, your earnings (the investment growth on those contributions) work differently. If you withdraw earnings before age 59½ and before meeting the five-year requirement, you’ll owe taxes and potentially a 10% penalty on those earnings.

Another significant benefit of Roth IRAs is that they don’t have required minimum distributions during your lifetime. You can leave the money growing tax-free for as long as you want, which creates excellent opportunities for estate planning and leaving wealth to your heirs.

Wrapping Up: Understanding the Differences Between a Roth vs. Traditional IRA

Choosing between Roth vs. traditional IRA accounts comes down to whether or not you want to pay taxes now or later. Both options can help you build long-term retirement savings, and the tax advantages of each can significantly boost your nest egg compared to taxable investment accounts.

Whether you’re drawn to the upfront tax break of a traditional IRA or the tax-free withdrawals of a Roth IRA, the most important step is getting started.

At California Credit Union, we’re committed to helping you reach your retirement goals with personalized guidance and competitive rates. As a member-owned financial institution, we put your interests first in ways that traditional banks simply can’t. Learn more about our IRA options can help secure your financial future.

References

- “Retirement Topics - IRA Contribution Limits.” Internal Revenue Service, www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits.

- “401(k) Limit Increases to $24,500 for 2026, IRA Limit Increases to $7,500.” Internal Revenue Service, www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500.

- 2026 Amounts Relating to Retirement Plans and IRAs, as Adjusted for Changes in Cost-of-Living, www.irs.gov/pub/irs-drop/n-25-67.pdf.