Understanding Credit Cards: What Age Can You Get a Credit Card?

Last updated on November 10, 2025

The typical age for getting your first credit card is 18 years old, but it isn't always that straightforward. While turning 18 opens the door to credit card applications, younger individuals have alternatives, and even 18-year-olds face certain restrictions that older applicants don't encounter. This article will uncover everything you need to know about credit card age requirements, from the legal basics to practical strategies for building credit at any stage of young adulthood.

What Is a Credit Card?

A credit card works by allowing you to borrow against a credit line for purchases, requiring you to repay whatever amount you've borrowed. When you use a credit card, you're borrowing against a predetermined credit limit set by the card issuer. This gives you access to a line of credit that can be used for purchases, cash advances, balance transfers and other transactions.

Each month, you'll get a statement showing your balance, minimum payment due and payment deadline. If you pay the full balance by the due date, you typically won't owe any interest. However, if you only make the minimum payment or carry a balance, you'll be charged interest on the remaining amount.

At What Age Can You Get a Credit Card?

The age requirement for credit cards is 18 years old in most states, as this is when you reach the age of majority and can enter into binding contracts. However, just because you can apply doesn't mean the process is identical to what older adults experience. While 18 is the standard age across most of the United States, it's worth noting that the age of majority varies slightly by state.

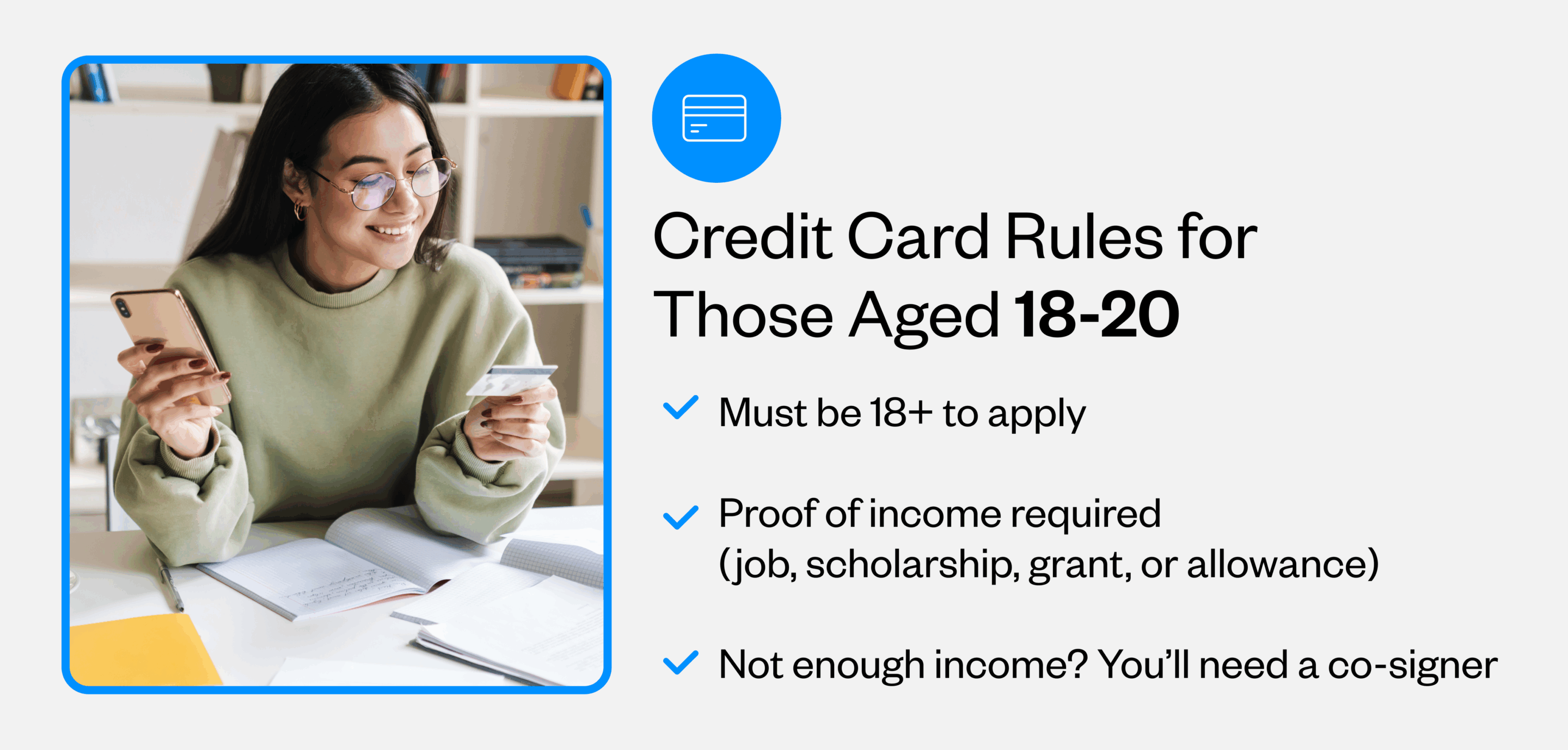

Credit Card Rules for Ages 18-20

The Credit CARD Act of 2009 created specific protections for young adults, particularly those between 18 and 20 years old. This federal legislation was designed to prevent credit card companies from targeting college students and young adults who may not fully understand the financial responsibilities associated with credit cards.

Under this act, if you're between 18 and 20, you must demonstrate independent income or have a co-signer (usually a parent or guardian) who agrees to take responsibility for the debt if you are unable to pay. The law defines acceptable forms of income broadly, encompassing wages from employment, financial aid refunds, scholarships, grants, allowances from family members and even monetary gifts. However, you need to be able to prove this income when applying.

The co-signer option allows parents or guardians to help young adults access credit while sharing the financial responsibility. Please note that missed payments or high balances will impact both the primary cardholder's and co-signer's credit reports.

Additional Credit Card Options for Those Under 21

If you're under 21 and don't meet the income requirements for your own credit card, you can become an authorized user on a parent or guardian's account. As an authorized user, you get your own card connected to someone else's account, allowing you to make purchases and begin building a credit history.

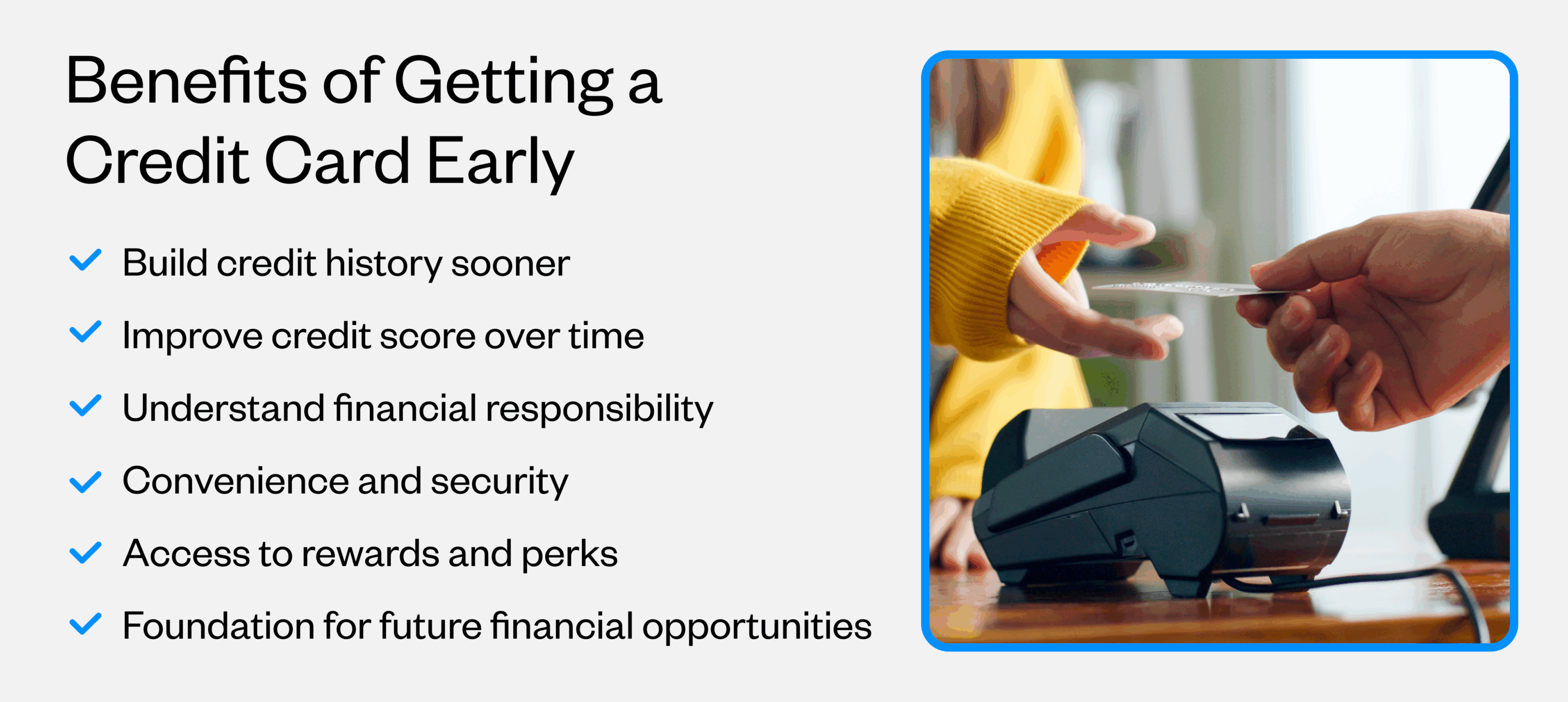

Benefits of Getting a Credit Card Early

Building credit as a young adult is a foundational step toward achieving financial goals. By understanding how credit cards work and taking proactive steps to establish a positive credit history, individuals can position themselves for success.

- Build credit history sooner: Your credit history length accounts for 15% of your credit score. Credit reporting agencies favor longer credit histories, so starting as soon as possible gives you a head start compared to waiting

- Improve credit score over time: Consistent, responsible credit card use can help you build and maintain a good credit score

- Understand financial responsibility: Using a credit card teaches valuable lessons about budgeting, interest rates and debt management.

- Access to rewards and perks: Many credit cards offer cash back, travel rewards or other incentives that can provide value when used responsibly

- Foundation for future financial opportunities: A strong credit history makes it easier to qualify for auto loans, mortgages, apartment rentals and sometimes even employment opportunities

Best Ways for Young Adults to Start Building Credit

Learning how to build credit as a young adult begins with understanding your options and selecting the approach that best suits your situation. Here are a few of the best ways for you to build credit:

- Share-Secured credit cards: The ideal credit card for those with very little credit history or those who may have a less than favorable credit background. At California Credit Union, this card links directly to your credit card secured savings account, providing the cash backing to secure your credit limit

- On-time payments: Whether you make payments on time (also known as payment history) makes up a large chunk of your credit score. Set up automatic payments when possible to ensure you never miss a due date

- Keep credit utilization low: Try to use less than 30% of your available credit limit, though under 10% is even better

- Monitor credit reports: You can use annualcreditreport.com to check your credit report and ensure accuracy.

- Understand credit basics: Take time to learn about interest rates, fees and how to build good credit habits that will serve you long-term

Start Building Credit With California Credit Union

Building credit doesn't have to be overwhelming when you have the right partner. California Credit Union offers a range of credit card options tailored to meet diverse needs and credit levels, from secured cards for credit building to rewards cards for established credit holders.

Understanding what age you can get a credit card is just the beginning of your credit journey. Whether you're 18 and ready for your first card, considering becoming an authorized user or helping a young adult in your life navigate these decisions, it's important to start with education and proceed with caution. As a member-focused institution, California Credit Union provides the personal attention and educational resources you need to make informed financial decisions.

By starting early, staying informed and choosing the right financial partner, you can build a strong credit foundation that will benefit you for decades to come. Consider the benefits of a credit union as you begin this important financial journey, and don't forget about opening your first bank account if you haven't already done so.