How to Get a Credit Card: A Complete Guide

Last updated on March 24, 2026

Learn how to get a credit card so you can begin building credit.

To get a credit card from a credit union, choose one that fits your financial needs, ensure you meet a few basic requirements (such as age and credit score) and submit an application with your personal, employment and income information. If approved, you’ll receive your credit card in the mail and can activate it using the instructions provided.

Key Takeaways

- You must be at least 18 to apply for a credit card in most states, and if you’re under 21, most issuers also require proof of independent income or a co-signer

- Your credit score is one of the most important factors issuers use when reviewing applications, and scores of 670 and above generally open up a broader range of card options with more competitive terms

- Secured, student, cash-back, low-interest and travel rewards cards each serve different goals, so choosing the right type before applying saves time and improves your chances of approval

- Submitting a credit card application creates a hard inquiry on your credit report, which often temporarily lowers your score by a few points

- If you’re denied, you’ll receive a letter explaining the reason and which credit bureau was used. You can use this information to address the issue and reapply when the timing is right

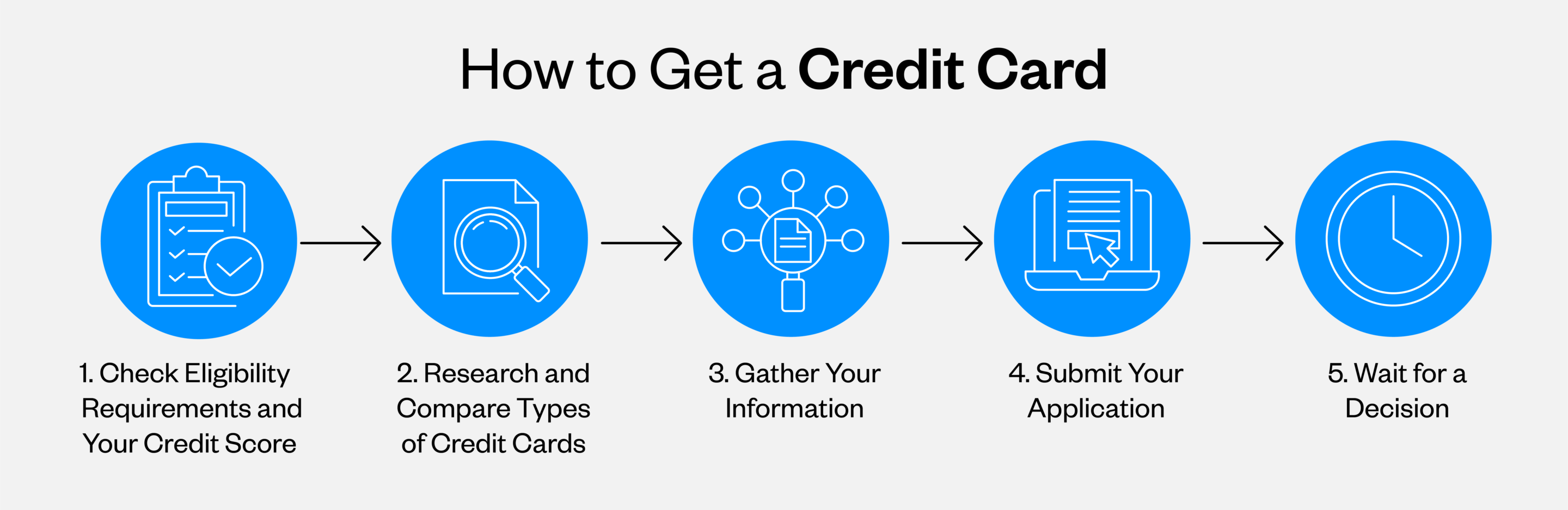

1. Check Eligibility Requirements and Your Credit Score

Before applying for a credit card, it helps to know what issuers are looking for. In most states, you need to be at least 18 years old to open a credit card in your own name. If you’re between 18 and 21, federal regulations typically require proof of independent income or a co-signer, since issuers can’t factor in household income without it.

Beyond age, credit scores play a major role in determining which cards you’ll qualify for and on what terms. Here’s how the general ranges break down:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very good: 740–799

- Exceptional: 800–850

Most standard credit cards require at least a fair credit score, while rewards and low-rate cards tend to favor applicants in the good to exceptional range. If you’re not sure where you stand, you can check your credit report for free at AnnualCreditReport.com, or learn more about what constitutes a good credit score here.

2. Research and Compare Types of Credit Cards

There are more types of credit cards out there than most people realize, and the differences between them go well beyond the card design. Before applying, take time to compare annual fees, interest rates (APR), rewards programs and any additional costs. It’s also worth looking at more than one type of financial institution — what a bank vs. a credit union offers can differ considerably in terms of rates, fees and member benefits. While researching credit card types, this is also a good time to think about the number of credit cards that make sense for your situation before you start applying.

Here are the most common credit union credit cards card to evaluate:

- Secured credit cards: These require a refundable cash deposit, which typically becomes your credit limit. They’re built for people with little or no credit history and report to the major credit bureaus just like a standard card, making them one of the most reliable ways to start establishing credit

- Student credit cards: These credit cards are for college students who are new to credit. They usually come with lower credit limits and more flexible approval requirements

- Cash-back credit cards: These return a percentage of what you spend — either as a flat rate on all purchases or at higher rates for specific categories like groceries, gas or dining. They’re well-suited for people who want consistent, predictable value from their card

- Low-interest credit cards: If there’s a chance you’ll carry a balance from time to time, a low-interest card limits what you pay in compound interest over time. Some also offer a 0% introductory APR for an initial period, which can be useful for a larger planned purchase

- Travel rewards credit cards: These earn points or miles on purchases, which can then be redeemed for travel expenses like airfare and hotel stays. They offer the most value for frequent travelers who can take full advantage of the redemption options.

3. Gather Your Information

Once you’ve settled on a card, the next step is pulling together everything you’ll need before filling out the application. Having it ready in advance keeps the process moving and reduces the chance of errors.

Here’s what most issuers will ask for:

- Personal information: Your full legal name, date of birth, current address and phone number

- U.S. residency or citizenship: Most card issuers require confirmation that you’re a U.S. citizen or permanent resident

- Social Security number: Used to verify your identity and pull your credit report as part of the review

- Income and employment details: Issuers want confidence that you can repay what you borrow. Be ready to share your employer’s name, your job title and your gross annual income, or your total annual income if you’re self-employed

- Monthly housing costs: Whether you rent or own, most applications ask for your monthly housing payment

- Bank account details or co-signer information: Some issuers may request a bank account number to verify financial stability. If you’re applying with a co-signer, have their information available as well

- Existing debts: Some applications ask about current loans or other financial obligations to get a more complete picture of your overall situation.

4. Submit Your Application

The application itself is typically quick. Most credit card issuers let you complete the entire process online in a matter of minutes. You’ll enter your information, review the card’s terms and submit. If you prefer not to apply online, many issuers also accept applications by phone or in person at a branch.

Before you submit, it’s useful to understand one thing that happens on your credit report. Credit card companies use a hard inquiry to check your credit report when you apply for a new credit card. Hard inquiries differ from soft inquiries — the kind that happen when you check your own credit — which do not affect your score at all. These credit inquiries can temporarily lower your score and stay on your report for up to two years. However, the impact is usually minor, but it’s a good reason to avoid submitting several applications in a short period of time.

5. Wait for a Decision

After you submit, many online applications return an instant decision. Others may take a few business days if the issuer needs to review your application more closely.

- Denial: If your credit application is denied, the issuer must legally send you an adverse action notice. This letter will outline the specific reasons, which might include a low or no credit score, insufficient income or too many recent applications. It will also identify which credit bureau was used to make the decision. You can then request a copy of the referenced credit report, look for issues like high balances or inaccurate entries, and address them before applying again. In some cases, starting with a secured card or one designed for fair credit is the smarter path forward

- Approval: If you’re approved, your card will typically arrive in the mail within a few business days. You’ll activate it online through the issuer’s mobile app or website, or by calling the number on the card. Once it’s active, you can start using it. Keep in mind that it’s important to know how to use a credit card responsibly before your first purchase so that you can get the most out of your card without falling into common traps like overspending or missing payments.

Start Smart: How to Get a Credit Union Credit Card

Knowing how to get a credit card is a starting point, but choosing the right one and using it responsibly over time is what supports your financial goals long term. If you’re still weighing your options, take time to review your credit score and think through which card type genuinely fits where you are financially right now.

California Credit Union offers a range of credit cards built around what members actually need, from low rates to cash-back rewards. Explore your options, and once your card arrives, set it up in a digital wallet so you can tap to pay, skip the card swipe and keep your purchases secure wherever you go.

Federally Insured by NCUA. Equal Housing Opportunity. View our Credit Card Disclosure.