Types of Savings Accounts: A Complete Guide

Last updated on May 8, 2026

Explore different types of savings accounts and see which one is right for you.

A savings account is a secure place to store money while earning dividends or interest over time, typically offered by credit unions and banks to help you build financial stability. Common types of savings accounts include regular savings or share savings accounts, high-yield savings accounts, money market accounts, share certificates and special savings accounts designed for specific goals.

Credit unions offer several types of savings accounts designed to help members grow their money. The right account depends on your goals, your timeline and how much access you need to your funds.

This guide breaks down the common types of savings accounts at a credit union and how to decide which fits your financial life.

Key Takeaways

- Credit unions typically offer higher dividend rates and lower fees than traditional banks, making them a strong choice for savers

- Share savings accounts are the most flexible option and work well for emergency funds or short-term goals

- Money market accounts and share certificates reward you with higher rates in exchange for larger balances or locking in your deposit

- IRAs give you a tax-advantaged way to save for retirement, with different benefits depending on whether you choose a Traditional or Roth option

- Specialty accounts like student savings, educator summer savings and business savings are built around specific needs and life stages

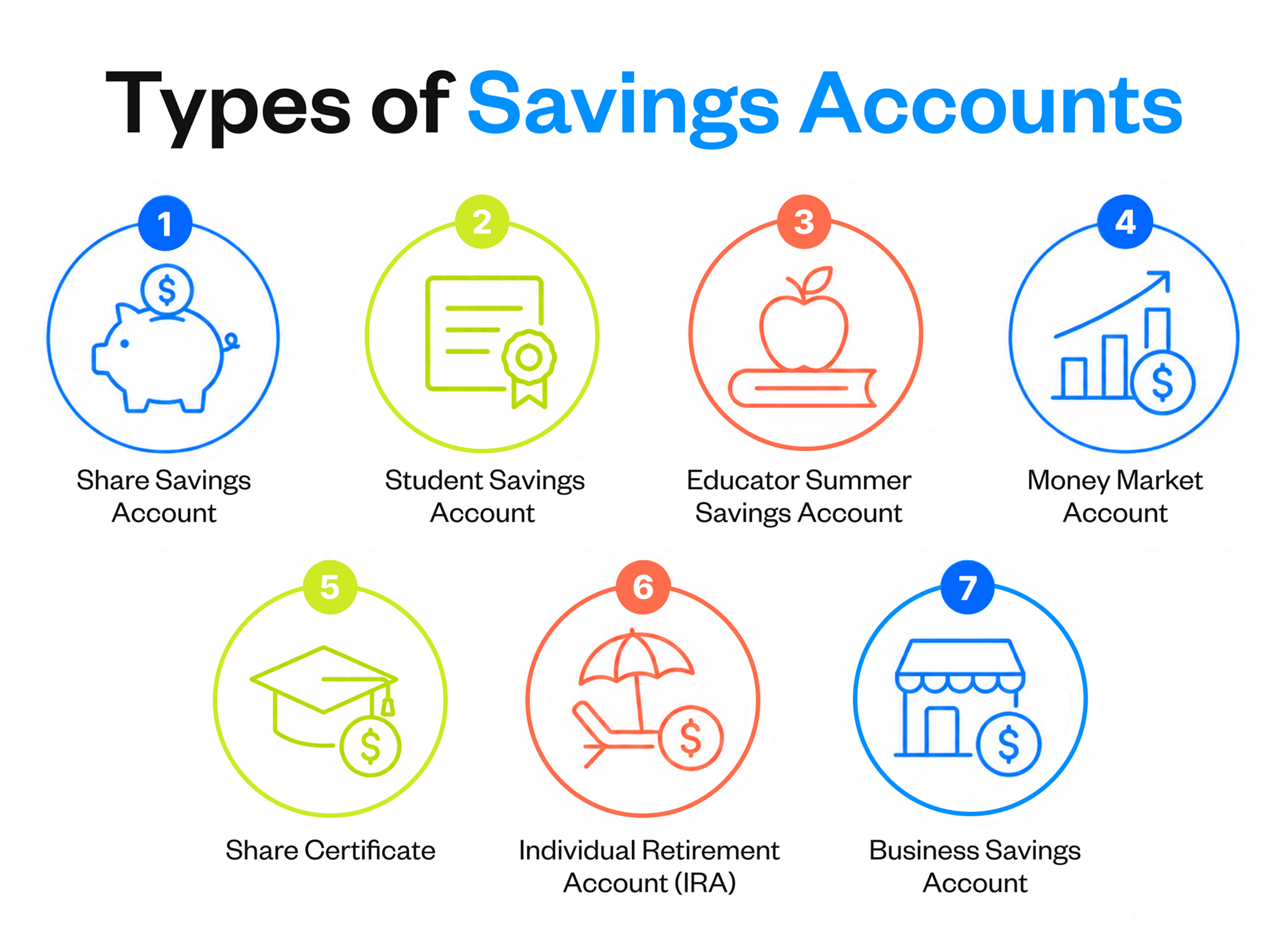

1. Share Savings Account

A share savings account is the foundational account at most credit unions. When you open one, you become a member and partial owner. It works like a traditional savings account offered by banks, where you deposit money, earn dividends and withdraw when needed. If you’re wondering how a checking vs savings account differs, savings accounts are built for holding and growing money rather than everyday spending.

Here’s what to know about share savings accounts:

Features | Low or no minimum balance, easy online and mobile access and interest rates that help your money grow |

Pros | Simple to manage with no complex rules, and your deposits earn compound interest |

Cons | Rates are lower than money market accounts or share certificates since you’re trading returns for full liquidity |

Best For | Anyone who wants a low-maintenance account for emergency savings or short-term goals |

2. Student Savings Account

Student savings accounts are designed for younger members learning to manage money. These accounts come with lower minimums and may include educational resources.

Here are the highlights of a student savings account:

Features | Low or no minimum deposit, no monthly fees in most cases and mobile banking access |

Pros | A low-pressure way to learn about saving and budgeting |

Cons | May have lower rate tiers compared to standard savings accounts |

Best For | Kids, teens and young adults building their first savings habits |

3. Educator Summer Savings Account

An educator summer savings account is built for teachers and school employees. It helps them set money aside during the school year for the summer months. Here’s what sets this account apart:

Features | Automatic payroll deductions during the school year, with funds disbursed over summer break |

Pros | Removes the guesswork from summer budgeting |

Best For | Teachers and school staff who want a structured way to prepare financially for summer |

4. Money Market Account

A money market account blends the earning potential of a savings account with some checking features like check-writing or debit card use. These accounts require a larger minimum balance but offer higher rates. Here’s what to know about money market accounts:

Features | Higher dividend rates than standard savings, potential check-writing access and tiered rates that reward larger balances |

Pros | You earn more while still having some flexibility to access funds |

Cons | Higher minimum balance requirements, and falling below that threshold may reduce your rate |

Best For | Savers with a larger balance who want better returns without fully locking up their money |

This comparison of a money market account vs. a savings account breaks down the differences. And if security is a concern, here’s a closer look at whether money market accounts are safe.

5. Share Certificate

A share certificate is essentially the credit union version of a bank’s certificate of deposit (CD). You deposit a set amount for a fixed term and earn a higher, locked-in rate. The tradeoff is that your money stays put until the term ends, or you’ll face an early withdrawal penalty. Here’s what to expect with a share certificate:

Features | Fixed rate for the entire term, terms typically range from 3 to 60 months and a guaranteed return |

Pros | Rates are usually higher than those of savings or money market accounts, and the fixed term protects you from rate drops |

Cons | Your money is locked in, and pulling it out early usually means a penalty |

Best For | People with money they won’t need for a set period who want a predictable, higher return |

6. Individual Retirement Account (IRA)

An IRA is a tax-advantaged account for long-term retirement savings. Credit unions offer both Traditional and Roth IRAs, and the right choice depends on your income and when you’d rather get the tax benefit. This guide on Roth IRA vs. Traditional IRA walks through the differences. Here’s what an IRA offers:

Features | Tax benefits on contributions or withdrawals depending on the type, annual IRS contribution limits and the option to hold your IRA as a savings account or certificate |

Pros | Helps retirement savings grow more efficiently through tax advantages, often with competitive credit union rates |

Cons | Contribution limits apply each year, and early withdrawals before age 59½ typically come with penalties |

Best For | Anyone planning for retirement who wants a tax-efficient way to save |

7. Business Savings Account

A business savings account gives business owners a dedicated place to set aside revenue, build a cash reserve, or save for future expenses. It also simplifies bookkeeping and tax filing by keeping business and personal funds separate. Here’s what a business savings account typically includes:

Features | Separate account for business deposits, competitive dividend rates and online banking access |

Pros | Keeps your finances organized, earns interest on idle cash and helps build a buffer for slower seasons |

Cons | May have minimum balance requirements, and some accounts limit monthly transactions |

Best For | Small business owners and freelancers who want to earn on reserves while keeping business and personal finances separate |

Benefits of Credit Union Savings Accounts

Credit unions are member-owned, not-for-profit institutions, and that structure directly affects what you earn and what you pay. Getting started is simple. Most credit unions let you open a bank account online in minutes, and this guide on what you need to open a bank account covers the process.

Here’s why credit union savings accounts stand out:

- Member-first structure: Profits go back into better rates, lower fees and improved services rather than to outside shareholders

- Stronger rates: Credit unions consistently offer higher dividend rates on savings, so your money grows faster with less working against you

- Personalized service: Credit unions tend to be community-focused, with staff who take time to understand your situation and help you find the right accounts.

For a deeper comparison, here’s how a bank vs. credit union stack up.

Wrapping Up: Choosing the Right Savings Account for Your Goals

The different types of savings accounts each serve a purpose, and the best approach often involves more than one. A share savings account handles everyday needs, while a share certificate or IRA helps you earn more on money you don’t need right away.

California Credit Union offers the full range of savings options covered in this guide — from share savings and money market accounts to share certificates, IRAs, student accounts, educator summer savings and business savings. Visit California Credit Union to explore which accounts align with your goals.