What Is a Roth IRA? A Complete Guide to Tax-Free Retirement Savings

Last updated on June 4, 2026

Learn what a Roth IRA is, how it works, contribution limits, tax benefits and whether it’s the right retirement account for you.

A Roth IRA is a type of individual retirement account that allows you to contribute after-tax income, invest those funds and make qualified withdrawals tax-free in retirement. Unlike traditional IRAs, where eligibility for an upfront tax deduction depends on an individual’s income, Roth IRAs do not offer a current-year tax deduction. Instead, they provide tax-free growth and tax-free withdrawals in retirement, provided IRS requirements are met.

Planning for retirement can feel overwhelming, especially when it comes to comparing different savings and investment accounts. This guide explains what a Roth IRA is, how it works, its tax advantages, contribution and withdrawal rules and how it compares to other retirement plans so you can decide whether it falls in line with your long-term financial goals.

Key Takeaways

- A Roth IRA is a retirement account funded with after-tax dollars that allows qualified withdrawals of contributions and earnings to be tax-free in retirement

- Roth IRAs offer benefits such as tax-free investment growth, no required minimum distributions (RMDs) and flexible access to original contributions

- Eligibility for a Roth IRA depends on IRS income limits, and annual contribution limits apply based on age and earned income

- Unlike traditional IRAs, where an upfront tax deduction may be available depending on an individual’s income, Roth IRAs do not offer a current tax deduction. Instead, they can provide long-term tax advantages, including tax-free retirement income

What Is a Roth IRA?

A Roth IRA is a type of individual retirement account that allows you to contribute money you’ve already paid taxes on and invest it for long-term retirement growth. In exchange for paying taxes upfront, qualified withdrawals in retirement are tax-free, including both your original contributions and investment earnings.1

For those learning how to save for retirement, a Roth IRA can be a great option if you want withdrawals to be free from federal income taxes in retirement. This structure can be especially valuable for people who expect to be in a higher tax bracket later in life or who want a predictable retirement income.

Roth IRAs can create significant long-term savings, especially for younger investors who have decades for their investments to grow. Paying taxes upfront may also help reduce uncertainty about future tax rates and provide greater flexibility when managing retirement income. Additionally, Roth IRAs allow account holders to withdraw their original contributions at any time without taxes or penalties, offering more flexibility than other retirement accounts.

Use our free retirement savings calculator to ensure you have enough money saved to fund your retirement years.

How Does a Roth IRA Work?

A Roth IRA works by allowing you to contribute after-tax income into a retirement investment account where your money can grow through tax-free compounding. Over time, earnings generated from investments such as stocks, mutual funds, ETFs or bonds can accumulate without being taxed each year, and qualified withdrawals in retirement are tax-free if IRS requirements are met. There are three main factors to consider when it comes to Roth IRAs, including contribution limits, income limits and withdrawal rules:

Roth IRA contribution limits

The Internal Revenue Service sets annual contribution limits for Roth IRAs and other types of retirement accounts, and those limits may change periodically to account for inflation. Contribution limits are based on age and earned income, meaning you generally must have taxable compensation to contribute.

For 2026, the contribution limit for Roth IRAs is set at $7,500, which is up from the 2024 and 2025 contribution limit of $7,000. Additionally, account holders aged 50 or older can make a catch-up contribution of $1,100, making the total contribution limit for 2026 $8,600.2

It’s important to note that the contribution limit applies across all IRA types. So, if you have both a Roth IRA and a traditional IRA, you can only make contributions up to the 2026 contribution limit of $7,500 for account holders under 50, not the annual maximum for each. For example, you can contribute $3,500 to a Roth IRA and $3,000 to a traditional IRA to reach the maximum of $7,500, but you can’t contribute $7,500 to a Roth IRA and $7,500 to a traditional IRA in the same year.

Roth IRA income limits

Eligibility to contribute directly to a Roth IRA depends on your modified adjusted gross income (MAGI) and tax filing status. As income increases, the amount you can contribute may gradually phase out until you become ineligible for direct contributions.

- Roth IRA income limits for single filers: For 2026, you must have a modified adjusted gross income (MAGI) of less than $153,000 to make full contributions to your Roth IRA if you’re a single adult. You can make partial contributions if your MAGI is between $153,000 and $168,000, and no contributions if your MAGI is $168,000 or higher.3

- Roth IRA income limits for married couples filing jointly: If you’re married filing jointly, you and your spouse can make maximum contributions if your MAGI is less than $242,000, and partial contributions if your MAGI is more than $242,000 and less than $252,000. If your 2026 MAGI is $252,000 or higher, you can’t contribute to a Roth IRA.3

- Roth IRA income limits for married couples living together filing separately: If you and your spouse lived with each other at any time during the year but are filing separately, your MAGI must be under $10,000 to contribute to a Roth IRA.3

Roth IRA withdrawal rules

One of the biggest advantages of a Roth IRA is the flexibility around withdrawals. Because contributions are made with after-tax money, you can generally withdraw your original contributions at any time without taxes or penalties.

However, withdrawing investment earnings follows different rules. To take earnings out tax-free and penalty-free, the withdrawal must be considered “qualified” by the IRS. In most cases, this means:

- You are at least 59 ½

- Your Roth IRA has been open for at least five years

Taking an early withdrawal before you reach the age of 59 ½ can result in a 10% penalty on withdrawn earnings, and if you withdraw from a Roth IRA that has been open for less than five years, the withdrawal will be considered a non-qualified distribution and may be subject to either a penalty, taxes or both.

The IRS does allow certain exceptions for early withdrawals, including qualified first-time home purchases, certain education expenses, disability or inherited IRA situations, which will be penalty-free but not tax-free.

What Are the Benefits of a Roth IRA?

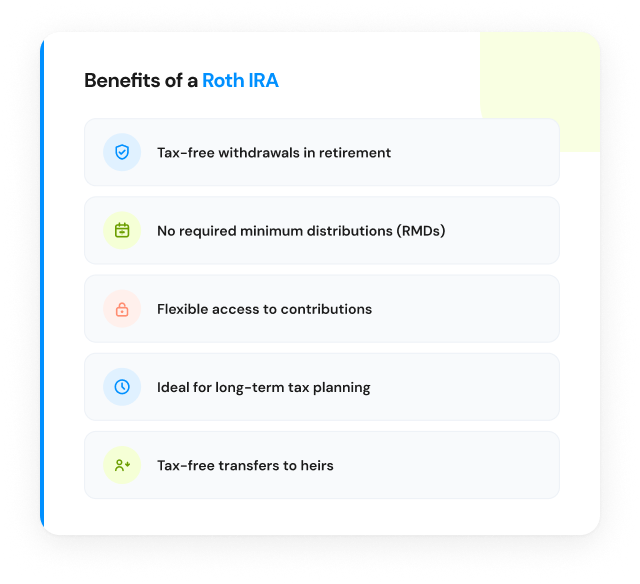

A Roth IRA offers several long-term advantages that can help investors build tax-efficient retirement savings and potentially reduce future tax burdens. Benefits of a Roth IRA include:

- Tax-free withdrawals in retirement: One of the biggest benefits of a Roth IRA is the ability to make qualified withdrawals tax-free in retirement. Because contributions are made with after-tax dollars, both your original contributions and investment earnings can typically be withdrawn without federal income taxes once IRS requirements are met

- No required minimum distributions (RMDs): Unlike many traditional retirement accounts, Roth IRAs do not require account holders to begin taking minimum distributions at a certain age during their lifetime, allowing investments to continue growing tax-free for longer and you to determine when and how you use your retirement savings

- Flexible access to contributions: Roth IRAs offer more withdrawal flexibility than many other retirement accounts. Since contributions are made with money that has already been taxed, you can generally withdraw your original contributions at any time without taxes or penalties, though different rules apply to investment earnings

- Ideal for long-term tax planning: A Roth IRA can help diversify your future tax situation and help with estimating your retirement income needs by providing a source of tax-free retirement income, which may be especially valuable for younger savers, individuals who expect to be in a higher tax bracket later in life or retirees looking to better manage taxable income during retirement

- Tax-free transfers to heirs: Roth IRAs can also provide estate planning advantages. While inherited Roth IRAs are still subject to distribution rules, beneficiaries can generally receive qualified distributions tax-free, allowing assets to pass to heirs with fewer tax consequences than some other retirement accounts

What Are the Differences Between a Roth IRA vs. Traditional IRA?

Roth IRAs and traditional IRAs are both tax-advantaged retirement accounts designed to help people save for the future, but they differ in how contributions, taxes, withdrawals and eligibility rules are handled. The main difference comes down to when you pay taxes: Roth IRAs are funded with after-tax dollars, while traditional IRAs may provide a tax deduction upfront but are taxed during retirement withdrawals.

Tax treatment

Roth IRAs are made with after-tax income, meaning you do not receive a tax deduction when contributing. In return, qualified withdrawals in retirement are generally tax-free.

Traditional IRA contributions may be tax-deductible depending on your income and workplace retirement plan participation. However, withdrawals in retirement are typically taxed as ordinary income.

Withdrawals

Qualified Roth IRA withdrawals are tax-free if IRS age and account requirements are met. Additionally, original Roth IRA contributions can generally be withdrawn at any time without taxes or penalties.

Traditional IRA withdrawals are taxed as income in retirement, and withdrawing funds before age 59½ may trigger taxes and penalties unless an exception applies.

Income limits

Roth IRAs have income eligibility limits that can reduce or eliminate your ability to contribute directly once your income exceeds certain thresholds.

Traditional IRAs do not have income limits for contributions, but higher earners may face limits on whether their contributions are tax-deductible.

Required minimum distributions

Roth IRAs do not require minimum distributions during the original account holder’s lifetime, allowing funds to continue growing tax-free for longer.

Traditional IRAs are subject to required minimum distributions (RMDs) beginning at age 72 (or 70½ if you turn 70½ in 2019), which means account holders must begin withdrawing a minimum amount annually.

Early withdrawals

Roth IRAs offer more flexibility for early access to contributions because contributed funds can generally be withdrawn at any time without taxes or penalties. However, withdrawing earnings early may result in taxes and penalties if the withdrawal is not qualified.

Traditional IRA early withdrawals are generally subject to both ordinary income taxes and a 10% early withdrawal penalty before age 59½, unless an IRS exception applies.

Use our free Roth vs. traditional IRA calculator to determine which account type aligns with your financial goals.

How Do You Open a Roth IRA?

Opening a Roth IRA is typically a simple process that can be completed online or in person through a financial institution.

- Choose a credit union, bank or brokerage: Select a financial institution that offers Roth IRAs and compare factors such as investment options, fees, account minimums and digital tools

- Complete the application: Fill out the Roth IRA application with your basic financial and contact information to establish the account

- Provide personal identification information: Most institutions require identification details, such as your Social Security number, date of birth, address and employment information to verify your identity

- Fund the account: Add money to your Roth IRA through a bank transfer, direct deposit, rollover or other eligible contribution method

- Select your investments: Once the account is funded, choose how you want to invest your money, such as mutual funds, ETFs, stocks, bonds or other retirement investment options

Wrapping Up: Start Saving for Retirement With a Roth IRA

A Roth IRA can be a valuable retirement savings tool if you’re looking to build tax-free retirement income, benefit from long-term investment growth and gain more flexibility over withdrawals and future tax planning. If you’re ready to start saving for retirement, explore our IRA options, including traditional and Roth IRAs, at California Credit Union.

All materials contained herein are for general informational purposes only and do not constitute tax or legal advice.

References

- Internal Revenue Service. (n.d.). Roth IRAs. https://www.irs.gov/retirement-plans/roth-iras

- Internal Revenue Service. (n.d.). Retirement topics – IRA contribution limits. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

- Internal Revenue Service. (n.d.). Publication 590-A (2025), Contributions to Individual Retirement Arrangements (IRAs). https://www.irs.gov/publications/p590a

- Internal Revenue Service. (n.d.). Retirement plans FAQs regarding IRAs. https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras