What Is Zelle®? A Complete Guide to How It Works

Last updated on June 3, 2026

Learn more about Zelle® and how it works.

Zelle® is a digital peer-to-peer payment service that lets users send and receive money directly between U.S. bank accounts, typically within minutes. Users can access Zelle® through participating bank or credit union apps or the Zelle® app by linking a bank account and sending money using a recipient’s email address or mobile phone number.

Zelle® is a popular digital payment service that’s commonly built into major banking and credit union apps and also available through its own mobile app, making it easy to transfer funds using just an email address or phone number. This guide explains what Zelle® is, how it works and what you should know about its fees, safety and best uses so you can decide when it makes sense to use it.

Key Takeaways

- Zelle® is a peer-to-peer payment service that sends money directly between eligible U.S. bank accounts, often within minutes

- Most banks and credit unions offer Zelle® inside their mobile banking apps, allowing users to send, request and receive money using only an email address or phone number

- Zelle® is typically free to use, but transfer limits and availability vary by financial institution and account type

- Zelle® is best for sending money to people you know and trust because payments are nearly instant, making them difficult to reverse

- California Credit Union offers digital banking tools and a Zelle® integration to make it easier to manage everyday payments, transfers and account activity in one place. Learn more here.

What Is Zelle®, and How Does It Work?

Zelle® is a digital payment service that allows people to send money directly between U.S. bank accounts, usually within minutes. It’s designed for fast, everyday transfers like paying friends, splitting bills or sending money to family without needing cash or checks.

Zelle® is owned and operated by Early Warning Services, a financial technology company that is itself owned by seven major U.S. banks, including institutions like Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank and Wells Fargo.1 Because it’s backed by this bank network, Zelle® is built directly into many banking apps, and it can also be used through the standalone Zelle® app.

Zelle® is only available in the United States and can only be used between U.S. bank accounts. This makes it different from traditional bank transfers, which often rely on ACH processing, which can take one to three business days to clear. Instead of moving money through an intermediary holding period, Zelle® transfers funds directly between participating banks, which is why payments are typically much faster.

How Do You Use Zelle®?

Sending and receiving money with Zelle® is fairly simple, especially if your bank or credit union already supports it. Most of the process happens inside your banking app, and once you’re set up, sending or receiving money takes just a minute or two.

- Enroll through your bank, credit union or Zelle® app: The first step is enrollment. Many banks and credit unions already have Zelle® built into their mobile banking apps, so you can sign up directly there. If your financial institution doesn’t offer it, you can use the standalone Zelle® app instead. Either way, you’ll be asked to connect your checking account so money can move in and out

- Add your email or phone number: Next, you’ll link an email address or mobile phone number to your account. This is what Zelle® uses to identify you and route payments. It’s always what other people will use to send you money, so it’s important you choose something you have regular access to

- Choose a recipient: When you’re ready to send money, you select a recipient using their enrolled email or phone number. If they’re already on Zelle®, their account will show up automatically. If not, they’ll get a notification prompting them to enroll before the transfer completes

- Enter amount and send: After selecting the recipient, you enter how much you want to send and confirm the payment. Most credit unions and banks will ask for a quick review step before finalizing the transfer. Once approved, the transaction is submitted instantly

- Recipient receives funds: If both sides are enrolled, the money typically arrives in minutes and goes straight into the recipient’s checking account. If the recipient hasn’t signed up yet, they’ll need to enroll first before they can access the funds.

Zelle® Fees, Limits & Transfer Speeds

Zelle® is designed for quick, everyday money transfers between people who already have U.S. bank accounts. While it’s generally known for being simple and low-cost, the exact fees, limits and timing can vary depending on the bank or credit union you use.

Fees

In most cases, Zelle® does not charge users any fees to send or receive money. Many banks and credit unions include it as a free digital banking feature inside their mobile apps. That said, some financial institutions may set their own rules for certain account types, so it’s always worth checking your bank or credit union’s specific terms. The standalone Zelle® app also doesn’t charge a fee for standard transfers.

Limits

Zelle® transfer limits are not set by the platform itself but by individual credit unions or banks. This means your daily and monthly sending limits can vary widely depending on where you bank. Some accounts may allow only a few hundred dollars per day, while others allow several thousand. New users often start with lower limits that may increase over time as the account relationship is established. Additionally, there is typically no limit on how often you can receive money through Zelle®.

Transfer times

Most Zelle® payments are delivered within minutes when both the sender and recipient are already enrolled. However, timing can vary in certain situations, such as when a recipient is new to Zelle®, transactions over a certain dollar limit or when a bank is reviewing a transaction for security reasons. In those cases, transfers may take one to three business days to complete. A notice of the applicable transaction time is presented to the sender before the transaction is processed.

Is Zelle® Safe?

Zelle® is generally considered safe for sending and receiving money to and from people you know and trust. Because it’s connected directly to U.S. bank accounts and operates through participating financial institutions, the platform uses bank-level encryption, fraud monitoring and account authentication to help protect transactions.

That said, Zelle®’s speed is also what creates risk. Payments are designed to move quickly and are often irreversible once completed. If you send money to the wrong person or authorize a payment to a scammer, recovering those funds can be difficult. Zelle® itself advises users to treat payments like cash and only send money to trusted participants.

A key distinction with Zelle® is the difference between fraud and scams. Unauthorized transactions, such as someone gaining access to your account without permission, may qualify for reimbursement protections under federal banking rules. But if you willingly send money because you were deceived by a scammer, banks or credit unions may classify the transaction as authorized, even if it was fraudulent in practice.

For most users, the safest way to use Zelle® is for personal transfers with people you already know, verify recipient information carefully and avoid using it for purchases from strangers or online marketplace transactions.

What Are Common Zelle® Scams?

Because Zelle® transfers are fast and usually irreversible, scammers often target users with schemes designed to create urgency or confusion. Many scams rely on convincing someone to willingly send money, which is why it’s important to know how these tactics work before using Zelle® for payments.

- Impersonation scams: With an impersonation scam, a fraudster will pretend to be someone you trust, such as your bank, a government agency, a utility company or even a family member. They may call, text or email you claiming there’s suspicious activity on your account and instruct you to “protect” your money by sending it through Zelle®

- Accidental payment scams: In this scam, someone claims they accidentally sent you money through Zelle® and asks you to send it back. The original payment may come from a stolen account or a fraudulent source. If you return the money manually, the initial transaction could later be reversed by the bank, leaving you responsible for the loss

- Marketplace fraud: Marketplace scams are common on online selling platforms and local marketplaces, where a scammer may pretend to buy an item, send a fake payment confirmation or pressure you to ship products before funds actually arrive. In other cases, sellers may accept Zelle® payments from buyers and disappear without delivering the item

To prevent yourself from falling victim to these scams, avoid using Zelle® for purchases from strangers, contact your bank or credit union directly using the number on your debit card or official website and use payment methods with buyer or seller protections for online sales whenever possible.

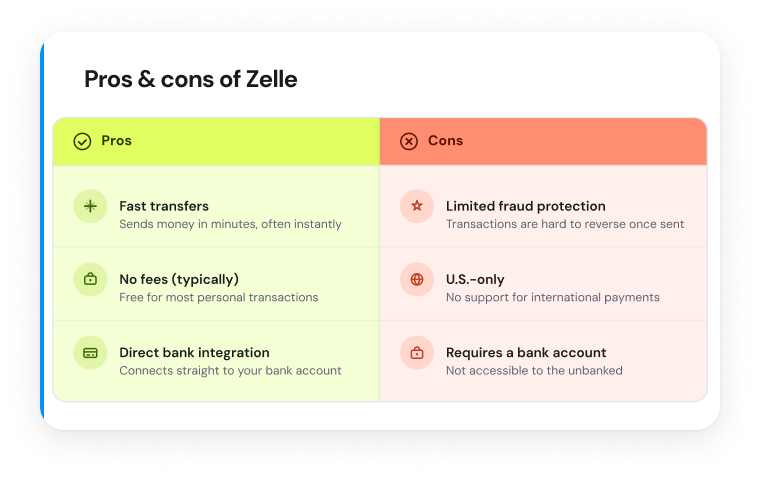

Pros and Cons of Zelle®

Zelle® is popular because it makes sending money quick and convenient, especially for everyday payments between people who already know each other. At the same time, the speed and simplicity can come with some tradeoffs that you should understand before relying on it for larger or riskier transactions.

Pros

- Fast transfers: Zelle®’s speed is one of its biggest advantages, as payments are often delivered within minutes when both users are enrolled, making it useful for splitting bills, paying roommates or sending money in time-sensitive situations

- No fees (typically): Most banks and credit unions offer Zelle® as a free service, so users can usually send and receive money without paying transfer fees, making it a convenient alternative to cash, checks and some other third-party payment platforms

- Direct bank integration: Unlike apps that hold money in a separate wallet or balance, Zelle® connects directly to participating credit union and bank accounts, and users can access it right inside their existing mobile banking app without needing another login or a standalone account

Cons

- Limited fraud protection: Zelle® payments are designed to move quickly and are difficult to reverse once sent. If you authorize a payment to a scammer or send money to the wrong person, recovering those funds can be challenging because the platform generally lacks traditional buyer protection features

- U.S.-only: Zelle® only works with eligible U.S. bank accounts, so it cannot be used for international money transfers. Users who need to send money abroad typically need a different payment service

- Requires a bank account: To use Zelle®, both the sender and recipient need a qualifying U.S. bank account or credit union account. This can limit accessibility for people who are unbanked or prefer prepaid cards and cash-based payment methods

How Does Zelle® Compare to Other Payment Apps?

Zelle is one of several popular peer-to-peer payment platforms available in the United States. While all of these apps allow users to send and receive money digitally, they work differently when it comes to transfer speed, payment protections, account structure and everyday use cases.

Feature | Zelle® | Venmo | Cash App | PayPal |

Primary Use | Bank-to-bank transfers | Social payments & digital wallet | Payments & financial tools | Online payments & purchases |

Transfer Speed | Usually minutes | 1-3 business days standard, instant option available | Standard or instant transfer options | Standard or instant transfer options |

Holds Money in App? | No | Yes | Yes | Yes |

Direct Bank Integration | Yes | Partial | Partial | Partial |

Buyer/Seller Protection | Limited | Limited | Limited | Yes, on eligible purchases |

International Transfers | No | No | Limited | Yes |

Fees | Usually free | Some instant transfer fees | Some instant transfer fees | Fees may apply depending on transaction |

Best For | Paying trusted contacts quickly | Splitting bills with friends | Flexible money management | Online shopping and business payments |

Zelle® vs. Venmo

Both Zelle® and Venmo let users send money to friends and family, but the way funds move through each platform is different. Zelle® transfers money directly between linked bank accounts, while Venmo uses a digital wallet system that can hold a balance inside the app before users transfer funds to their bank.

What is a digital wallet? It’s essentially an app-based system that stores payment information and allows users to hold, send or spend money electronically without moving funds directly between bank accounts every time. Venmo is often more social and consumer-oriented, with features like payment notes, public transaction feeds and debit card options. Zelle® is more bank-focused and tends to feel closer to a traditional banking experience.

Zelle® vs. Cash App

Cash App offers broader financial features than Zelle®, including debit cards, investing, stock purchases and even Bitcoin transactions. Zelle®, by comparison, focuses almost entirely on direct bank-to-bank payments. Both platforms support fast money transfers, but Cash App users often maintain a stored balance inside the app, while Zelle® sends funds directly to a linked checking account.

Zelle® vs. PayPal

PayPal has been around longer than Zelle® and supports a wider range of online payments, including business transactions, e-commerce purchases and international transfers. Zelle® is more limited in scope and is primarily intended for personal payments within the United States.

One of the biggest differences is buyer and seller protection. PayPal offers dispute resolution and purchase protection on many transactions, making it more suitable for online shopping and marketplace payments. Zelle® generally does not provide these protections, which is why it’s best used only with people you know and trust. PayPal can also involve transfer fees depending on the payment type, while Zelle® is usually free through most participating banks and credit unions.

Wrapping Up: Getting Started With Zelle®

Zelle® has become one of the most widely used peer-to-peer payment services because it makes sending money fast, simple and convenient through participating banks and credit unions. Whether you’re splitting bills, paying someone you trust or transferring funds quickly, understanding how Zelle® works, its limitations and common scams can help you use it more confidently and securely. To learn more about using Zelle® or how to open a bank account to start using Zelle, explore our credit union banking options and digital banking features.

References

- Early Warning Services, LLC. (n.d.). Consumer reporting companies list. Consumer Financial Protection Bureau. https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/consumer-reporting-companies/companies-list/early-warning-services-llc/