How to Improve Your Credit Score: A Complete Guide

Last updated on March 24, 2026

Discover tips and best practices on how to improve your credit score.

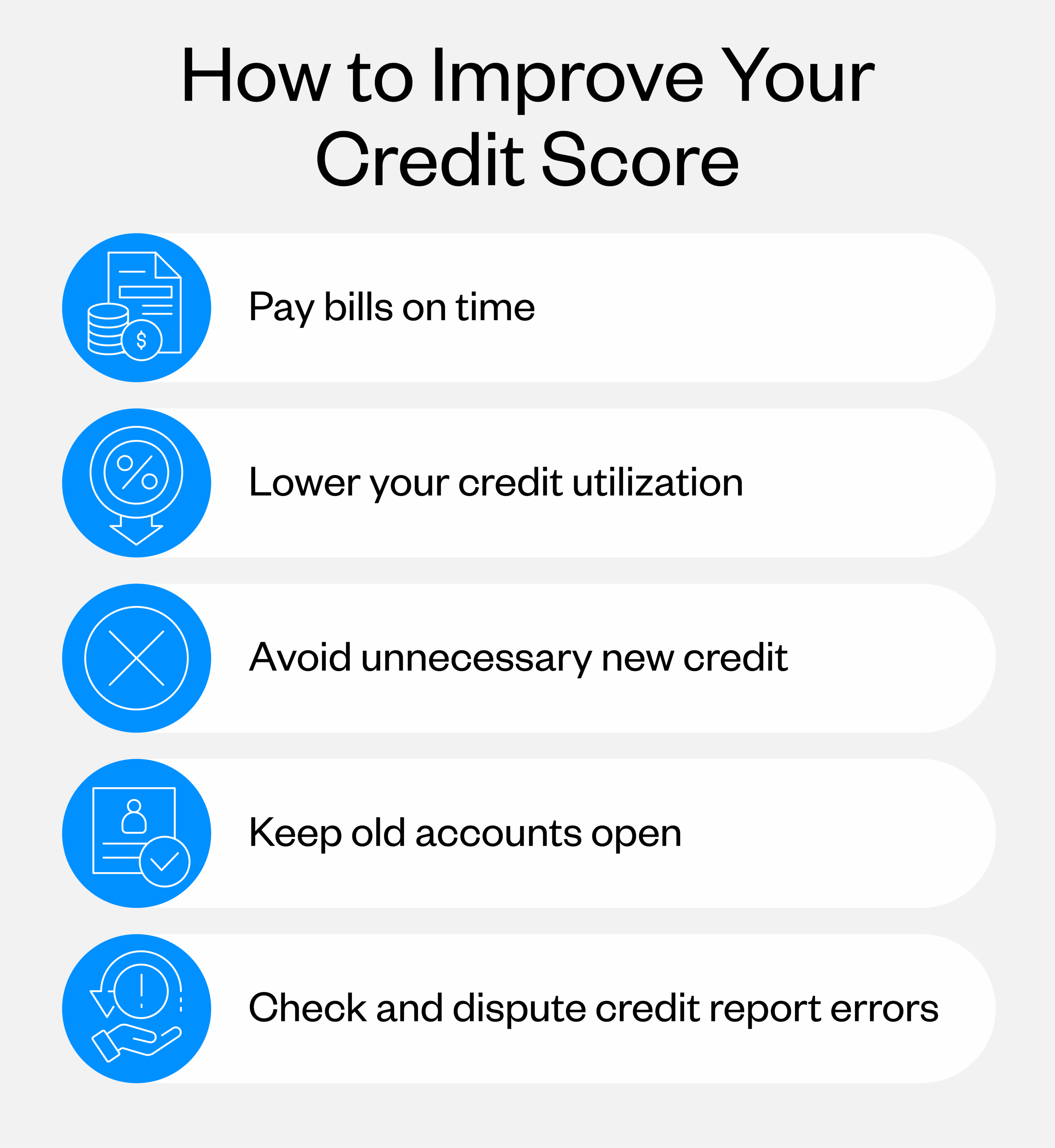

To improve your credit score, make sure to make on-time payments each month, keep your credit utilization low, typically below 30%, avoid unnecessary new credit, keep old credit accounts open and check and dispute credit report errors.

This guide breaks down how credit scores work, what factors influence them and what you can do to improve your own over time.

Key Takeaways

- Payment history makes up the largest portion of your credit score, and even a single missed payment can cause a significant drop. Autopay and payment reminders are two of the most reliable ways to stay on track

- Keeping your credit utilization below 30% — or closer to 10% — can improve your score relatively quickly. Paying down balances or requesting a higher credit limit are both effective approaches

- Inaccurate or outdated information on your credit report can drag your score down. Checking regularly and disputing mistakes is a step worth taking

- Short-term wins are possible, but building steady credit habits over months and years is what produces real, lasting results

What Is a Credit Score?

A credit score is a number that reflects how reliably you manage borrowed money. Lenders use it to decide whether to approve your loan or credit applications and what interest rates to offer you. The higher your score, the less risk you represent.

The two most widely used scoring models are FICO and VantageScore. FICO is the standard for mortgage and auto loan decisions, while VantageScore, which was developed collaboratively by the three major credit bureaus, is used widely by credit card issuers and financial apps. Both models use the same 300-850 scale and are driven by the same underlying behaviors.

Understanding how credit scores work is necessary for knowing how to improve yours over time.

What Is a Good Credit Score?

What’s considered a good credit score depends on which model is being used — and FICO and VantageScore don’t draw the lines in exactly the same place. Here’s how each one breaks down:

- Very poor (VantageScore only: 300–499): VantageScore breaks out this tier separately; FICO folds it into Poor. Either way, approval is unlikely with most traditional lenders, and credit options are extremely limited

- Poor (FICO: 300–579 | VantageScore: 500–600): A poor credit score can make it difficult to qualify for most loans or credit cards. If approved, expect higher rates and limited options

- Fair (FICO: 580–669 | VantageScore: 601–660): Some products may be available, but costs are typically higher. Consistent effort at building good credit can move you up significantly within a year or two

- Good (FICO: 670–739 | VantageScore: 661–780): Most lenders view you as a lower-risk borrower at this level. You’ll have access to more options at more competitive rates

- Very good / Exceptional (FICO: 740–799 / 800–850 | VantageScore: 781–850): FICO splits the top into two tiers; VantageScore calls everything above 781 Excellent. Either way, borrowers here qualify for the best available rates and terms

Credit scores update as new information is reported to the bureaus, which is usually once a month. Changes to your habits can start showing up in your score within 30 to 45 days, though some improvements take longer.

What Factors Affect Your Credit Score?

Your score reflects several behaviors working together. Here are the five main factors and how they’re weighted:

- Payment history: This is the heaviest single factor, making up 35% of your FICO score. Late payments stay on your report for several years

- Credit utilization ratio: This number measures how much of your available credit you’re currently using, accounting for about 30% of your score. Most experts recommend staying below 30%, with under 10% being ideal

- Length of credit history: The longer your accounts have been open, the better. This includes the age of your oldest account, your newest account, and the average across all accounts

- Credit mix: Having a mix of account types, such as credit cards, auto loans, student loans and a mortgage, shows credit issuers and lenders you can handle different kinds of debt. This factor carries less weight but still counts

- New credit inquiries: Each time you apply for new credit, a hard inquiry is added to your report. Too many in a short window can suggest financial strain and temporarily lower your score

How to Improve Your Credit Score

Knowing how to increase your credit score means knowing which steps carry the most weight. Some of the ones below will show results faster than others, depending on what’s currently dragging your number down. Here are a few ways to improve your credit score:

Pay bills on time

Payment history carries more weight than anything else in the credit scoring formula. A payment that’s 30 or more days late can cause a significant, lasting drop that stays on your report for seven years.

Here are a few tips to help you stay current on your bills:

- Set up autopay: Automating at least the minimum payment ensures you never miss a due date. If your budget allows, pay more than the minimum on any credit cards because carrying a balance costs you in compound interest over time

- Use payment reminders: Most banks and credit unions let you set text or email alerts through their apps. A reminder a few days before your due date can prevent a costly slip

- Pay at least the minimum when funds are tight: When money is tight, paying the minimum is still enough to protect your payment history. A payment only becomes a problem once it’s 30 or more days past due — that’s when it gets reported as late and can cause real damage to your score

Lower your credit utilization

Part of learning how to use a credit card responsibly is knowing how much of your available credit you’re actually using at any given time. Your credit utilization ratio is the percentage of your total available credit you’re using. Staying below 30% is the widely cited benchmark, but getting closer to 10% or under produces stronger results.

Here are a few ways to bring that number down:

- Pay down existing balances: This is the most direct route. Card issuers typically report your balance on your statement closing date, so paying before that date lowers what gets reported to credit reporting agencies

- Make multiple payments per month: Spreading payments across the billing cycle can reduce your average reported utilization

- Request a credit limit increase: If you’ve maintained an account responsibly, a higher limit reduces your utilization ratio, as long as your spending stays flat

Avoid unnecessary new credit

Every new credit application triggers a hard inquiry on your report. A single inquiry typically has a minimal effect, but multiple in a short window can suggest financial instability to lenders. Hard inquiries stay on your report for two years, though their scoring impact fades after about 12 months.

Keep in mind that opening new credit isn’t always the wrong move. For instance, consolidating debt or securing better terms can justify having a few hard inquiries on your credit report. Just make sure each decision is deliberate.

Keep old accounts open

The length of your credit history plays a bigger role in building good credit than most people realize. When you close an older account, you shorten your average account age, which can pull your score down even when everything else looks fine.

There are cases where closing an account makes sense, like if one has a high annual fee you’re no longer getting value from, or you have an account that’s making it too easy to overspend. Outside of that, keeping older accounts open is usually the better move. The same logic applies to the number of credit cards you have. In general, closing several at once tends to do more damage than simply leaving them open and using them occasionally.

Check and dispute credit report errors

Errors on credit reports are more common than most people expect. Payments reported incorrectly, accounts that don’t belong to you, or outdated negative marks can all bring your score down without cause.

You’re entitled to a free report from each of the three major credit reporting bureaus (Experian, TransUnion, and Equifax) through AnnualCreditReport.com. Review all three, since not every creditor reports to all of them. If you find an error, file a dispute directly with the bureau that’s reporting it. Correcting a legitimate mistake can improve your score faster than most other steps.

How Long Does It Take to Improve a Credit Score?

There isn’t a one-size-fits-all timeline for improving your credit score. Someone correcting a reporting error will see results much faster than someone recovering from a string of missed payments. Here’s a general breakdown of what to expect:

- Short-term improvements (30–60 days): Paying down a high balance or correcting a credit report error can show results within one to two billing cycles

- Medium-term improvements (3–6 months): Consistent on-time payments and controlled utilization will register more noticeably over several months of steady behavior

- Long-term credit rebuilding (6–24 months): Recovering from serious negative marks like late payments, collections, or high balances takes time. Steady habits over a year or more are what produce lasting improvement

Wrapping Up: Build Your Credit Score Step-by-Step

Improving your credit doesn’t require a dramatic overhaul, but you do need to build consistent habits. Pay bills on time, keep your balances low, avoid unnecessary credit applications and check your report regularly for errors. Small, steady actions are what help improve credit scores over time.

If you’re ready to take the next step, California Credit Union has the tools to help you get there. Whether you’re learning how to save money alongside building credit, curious about the benefits of choosing a bank vs. a credit union or looking for a smarter way to manage your spending with a digital wallet, California Credit Union offers resources designed to support your financial goals.